Brief overview of treatment

As part of Action 13 to re-examine transfer pricing documentation, the Slovak Republic signed along with thirty other countries a document on automatic exchanging of information – “Country-by-country (CbC) reporting” – on 28 January 2016. CbC reporting rules apply to large multinationals with consolidated annual turnover above 750 million EUR. These multinationals will annually report information to the relevant tax authority in their Member State. The tax authorities in the Member States will then automatically exchange this information on the global allocation of income, profits, capital, employees and property, and also information about taxes paid. These CbC reporting rules should enable tax authorities in these Member States to detect easier any discrepancies in the multinationals’ transfer pricing as well as any related tax evasion.

Current situation

On 1 February 2017, the National Council of the Slovak Republic passed a law on international assistance and cooperation in tax administration, which comes into force on 1 March 2017. Given the effective date, we believe the treatment to be valid when filing tax returns for the 2016 fiscal year.

Who is covered by the treatment? What are the duties of individual parties?

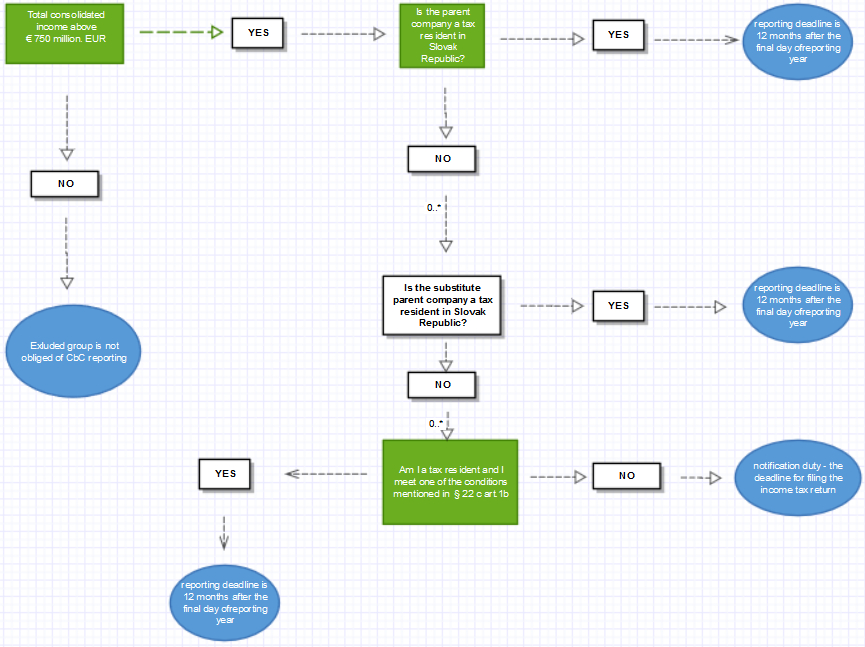

Who is covered by the tax treatment and what obligations they have is captured in the diagram below. These rules also require identification of the reporting entity. What is important is that it covers every member of a multinational (not just a separate legal entity but under certain conditions even a branch office or a permanent establishment) with consolidated revenues above € 750 million EUR.

Reporting and notification deadline

The reporting deadline in different countries is 12 months after the final day of the multinational’s reporting year. The reporting is first filed for 2016 if it is going to be filed by the parent. If another entity files the report, 2017 will be the first year for which it will be filed. The deadline for filing the notification is the deadline for filing the income tax return for the reporting year. The form is available in the electronic form section of the Financial Administration’s website: https://pfseform.financnasprava.sk/Formulare/eFormVzor/INE/form.378.html

Penalties

The penalty is up to € 10,000 for failure to file the report in each country and up to € 3,000 for failure to file the notification.